Article

How to Design Flexible Investment Loan Structures for Smarter Gearing

A practical guide to structuring investment loans so your gearing stays flexible as rates, tax rules and your portfolio change. Covers cross-collateralisation, standalone loans, offsets, splits and real-world scenarios.

Key Takeaway

This guide explains how Australian investors can design flexible investment loan structures by prioritising standalone securities, using multiple offsets, and keeping clear separation between deductible and non‑deductible debt. It highlights that cross‑collateralisation can trap equity and limit refinancing, and that 3–6 months of repayments in offset buffers improves resilience. Actionable steps include mapping all loans, securities and purposes, and planning staged restructures to protect serviceability, tax outcomes and gearing flexibility.

Designing investment loan structures that keep your gearing flexible means arranging your loans, securities and offsets so you can adapt as interest rates, tax rules and your life change. It’s about separating risks, keeping equity accessible, and making future moves (buy, sell, refinance, debt recycle) as frictionless as possible, while staying within lender and ATO rules.

In practice, that usually means favouring standalone loans over cross‑collateralisation, matching each loan to a specific security and purpose, and using offsets and loan splits deliberately – not just taking whatever structure the bank suggests.

1. What “flexible gearing” actually means in Australia

1.1 A working definition

For Australian property investors, flexible gearing is the ability to:

- Adjust your leverage up or down without forced sales.

- Refinance or switch lenders when policy or pricing changes.

- Buy or sell individual properties without disturbing the whole portfolio.

- Keep tax‑deductible and non‑deductible debt clearly separated.

Loan structure is the plumbing that makes this possible – or impossible.

1.2 Why structure matters more as the rules tighten

The 2026–27 Federal Budget and follow‑on legislation are reshaping negative gearing and CGT for residential investors. In summary (based on Treasury and Budget papers):

- From 1 July 2027, negative gearing for residential property will generally be limited to new builds.[1–3, 10–11]

- Established residential properties bought after 7:30pm 12 May 2026 will have rental losses largely quarantined – they can’t be offset against salary or other non‑rental income from 1 July 2027.[8, 15, 17–18]

- Existing properties held before that time are grandfathered under the old rules while you own them.[7, 9, 20]

That means:

- Your tax position by property will diverge – some can still be negatively geared in the old sense, others can’t.

- You may lean more towards new builds or commercial/other assets for future purchases.

- Structuring loans per property and per purpose becomes even more important so your accountant can track deductions accurately and you can adapt as rules evolve (see also /insights/self-employed-business-owners-high-income-professionals-negative-gearing-cgt-strategy).

1.3 The three big goals of flexible structures

Most investors should design towards three outcomes:

- Control – can you choose which property to sell, refinance or debt recycle next?

- Access – can you reach your equity without triggering a portfolio‑wide reassessment or new LMI?

- Resilience – can you ride vacancies, rate rises or income shocks without fire‑selling assets?

The rest of this guide is about the levers you can pull to get there.

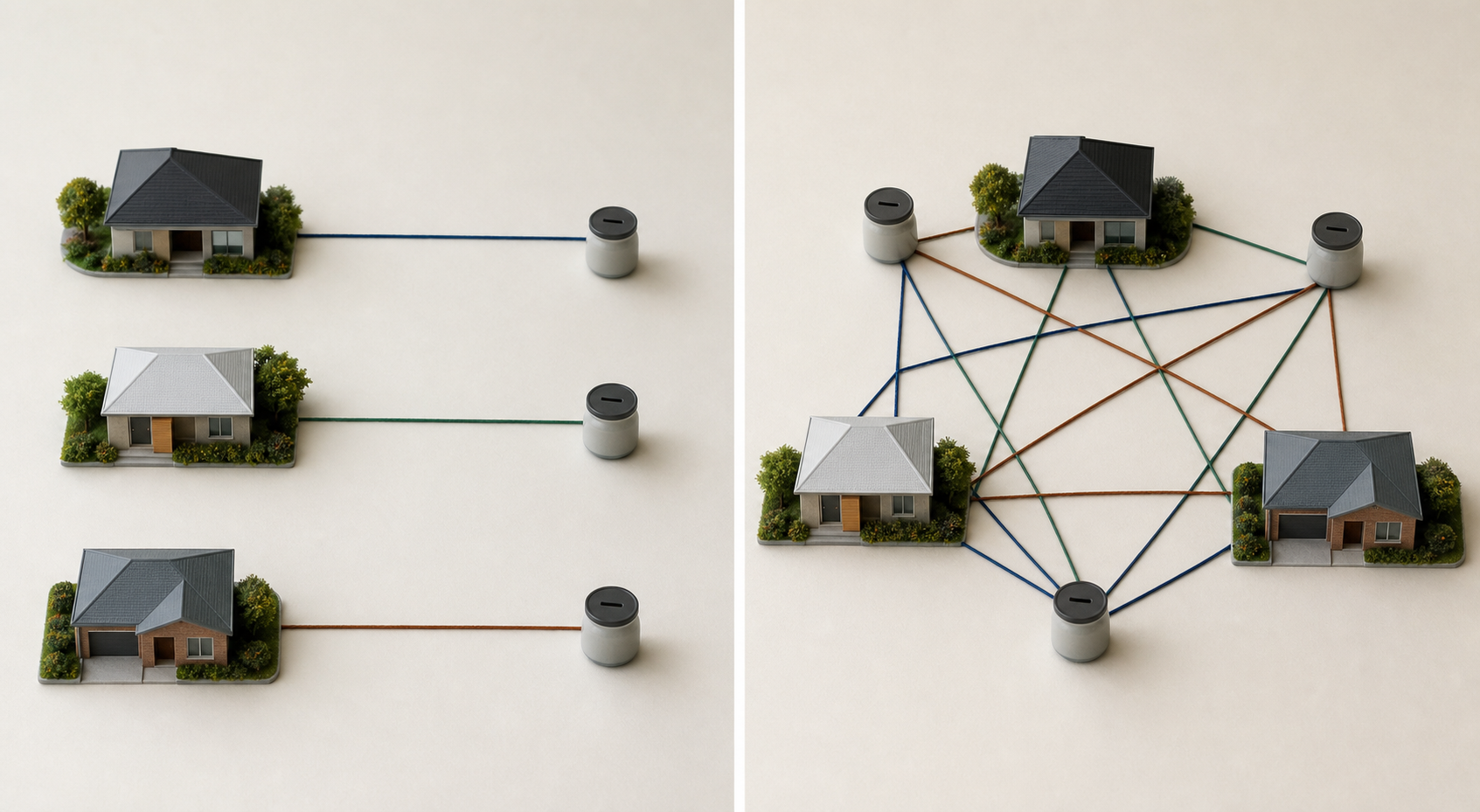

2. Standalone vs cross‑collateralised structures

2.1 What each structure actually looks like

Standalone (single security) loans

- Each property secures its own loan (or set of splits).

- The lender’s mortgage over Property A only secures debt related to Property A.

- Equity access and decisions can be made property by property.

Cross‑collateralised loans

- Two or more properties secure one or more loans together.

- Your home and multiple investments all sit under one big security pool.

- Changing one part often triggers a reassessment of everything.

See our cross‑collateralisation deep dive: /insights/unwinding-cross-collateralisation-complex-securities.

2.2 Why standalone usually wins for geared investors

Cross‑collateralisation isn’t always evil, but it typically reduces flexibility:

- Equity trap – big rises in one property’s value can be soaked up supporting weaker properties.

- Refinance friction – moving one loan to a sharper lender can require wholesale restructuring.

- Forced linkage – selling one property may require part‑repayment of other loans to keep portfolio LVRs inside policy.

By contrast, standalone structures usually give you:

- Cleaner LVR and equity clarity by property.

- Easier piecemeal refinancing if another bank will take a single asset.

- Less admin when rebalancing your portfolio.

2.3 Worked example: cross‑collateralised vs standalone

Assume:

- Home value: $1,200,000, loan $600,000.

- Investment A: $800,000, loan $640,000.

- Investment B: $700,000, loan $560,000.

Scenario 1 – cross‑collateralised pool

Total value $2.7m, total debt $1.8m – overall LVR ~67%.

You want to sell Investment B to reduce non‑deductible home debt.

- Lender may insist that some of the sale proceeds go to keep the overall LVR at policy levels.

- That can mean less cash to move against your home loan and a slower path to debt recycling.

Scenario 2 – standalone loans

Each property at ~75–80% LVR with its own loan.

- Sell Investment B, pay out its loan.

- Net sale proceeds after costs are yours – you can choose to reduce home debt or fund the next deposit.

The cashflow is very different even though the asset mix is identical.

2.4 Summary comparison table

| Feature | Standalone loans | Cross‑collateralised loans |

|---|---|---|

| Each property secures… | Only its own loan(s) | Multiple loans across multiple properties |

| Equity access | Clear by property, easier to release | Blended, may be trapped in portfolio |

| Refinancing individual loans | Usually straightforward | Often complex, may require multi‑property moves |

| Selling a single property | Proceeds mostly free once its loan repaid | Lender may demand extra debt reduction elsewhere |

| Admin/complexity over time | More loans to track but clearer purposes | Fewer accounts, harder to untangle later |

| Flexibility under policy/tax changes | High | Low to medium, depends on lender willingness |

If you’re already crossed up, see our step‑by‑step guide: /insights/unwinding-cross-collateralisation-complex-securities.

3. Offsets, splits and repayment types for flexible gearing

3.1 Using offsets the right way as an investor

An offset account reduces interest on the linked loan balance while keeping your cash liquid. For geared investors, they’re a core flexibility tool.

Key principles:

- Match offsets to non‑deductible or likely‑to‑become‑non‑deductible debt first (typically your home loan).

- Where possible, keep separate offsets for different purposes (e.g. personal cash vs future investment deposits) so your accountant can track the source of funds.

- Aim to hold at least 3–6 months of total loan repayments across your offsets as a resilience buffer.[16]

This buffer materially reduces the risk of forced sales during vacancies, higher RBA cash rates or temporary income loss.

3.2 Loan splits: keeping purposes clean

Splitting a loan into sub‑accounts lets you:

- Match each split to a single purpose (e.g. original purchase, renovations, equity released for shares).

- Run different repayment types or rates on different splits.

- Recycle debt in stages without confusing deductible and non‑deductible balances.

For example, a $900,000 home loan might be split as:

- Split 1: $600,000 – original purchase, P&I, primary offset.

- Split 2: $300,000 – investment equity release, IO, separate offset used only for investments.

As you debt recycle (see /insights/debt-recycling-tax-effective-loan-structuring-australia), you can pay down Split 1 aggressively while re‑drawing or using available limit in Split 2 for investments, maintaining deductibility.

3.3 P&I vs interest‑only for investors

Principal & interest (P&I) repayments:

- Reduce debt over time, improving your future borrowing capacity and resilience.

- Are usually priced lower than investment interest‑only (IO) rates.

Interest‑only (IO) repayments:

- Reduce repayments in the short term, improving cashflow.

- May cost more in rate and total interest over life of the loan.

A flexible structure often uses P&I on your home loan and carefully targeted IO on investment splits for defined periods, with a plan for what happens when IO expires.

3.4 Worked cashflow example

Assume:

- Investment loan $700,000 at 6.5% p.a.

- 30‑year term.

P&I repayment ≈ $4,430/month.

IO repayment ≈ $3,792/month.

That $638/month difference can:

- Support your cashflow if you’re early in portfolio building, or

- Be directed to smash down your home loan P&I, accelerating the shift from non‑deductible to deductible debt.

The right choice depends on your overall plan, tax position and risk tolerance – not just minimising today’s repayment.

4. Designing per‑property structures in a geared portfolio

4.1 Match each loan to a single primary security

For most investors, a clean base case is:

- One property = one primary loan (with splits as needed).

- Home/semi‑PPOR: focus on P&I, big offset, no cross‑collateralisation.

- Each investment: loan(s) secured predominantly by that property.

If you use your home equity to fund an investment deposit, try to house that equity release in a separate investment‑purpose split on the home loan, not jumbled together with your original owner‑occupied borrowing.

4.2 Keep tax‑deductible and non‑deductible debts separate

ATO rules focus on the purpose of the borrowing, not the security alone. But muddled loan accounts make it much harder to evidence purpose.

Good practice:

- Separate loan splits for: home purchase, home renovations, investment deposits, investment renovations, business use.

- Don’t mix personal expenses with investment redraws in the same account.

- Use dedicated offsets for investment cash vs personal cash where the lender allows.

This becomes crucial as negative gearing rules diverge between grandfathered established properties and post‑2026 acquisitions.

4.3 LVR bands and when to push leverage

In broad terms (actual limits vary by lender and policy):

- ≤80% LVR – often avoids LMI, usually easier for future refinancing.

- 80–90% LVR – LMI payable; acceptable if strategy is growth‑focused and buffers are strong.

- >90% LVR – niche strategies only; very tight on cashflow and future flexibility.

Flexible structures often:

- Aim for ≤80% LVR on the home over time.

- Accept higher LVRs on certain investments where growth prospects and income are strong.

- Use extra repayments and debt recycling to steadily shift total debt towards the more tax‑effective side.

For more on juggling LVRs as you grow, see /insights/restructuring-loans-growing-property-portfolios.

4.4 Example: three‑property geared portfolio

Assume:

- PPOR: $1.5m value, $750k loan (P&I, big offset).

- Investment 1 (grandfathered established): $900k value, $680k loan.

- Investment 2 (new build, post‑2026): $850k value, $680k loan.

A flexible structure could be:

- PPOR loan split A: $600k (original purchase), P&I, main offset.

- PPOR loan split B: $150k (investment equity release for future deposit), IO, separate offset used only for investment purposes.

- Invest 1: standalone 80–85% LVR loan, P&I or IO depending on cashflow.

- Invest 2: standalone 80–90% LVR loan, IO for first 5 years while you stabilise rent.

You now have three separate security positions, plus clear tracking for the equity released from the home. If policy tightens on one property type, or if you later want to refinance Invest 2 to a different lender, you’re not forced to move or re‑document the whole portfolio.

5. Aligning loan structure with tax, estate and policy risk

5.1 Negative gearing reforms and portfolio design

Given the post‑2026 changes:

- Existing grandfathered properties may still justify higher gearing if cashflow allows, as losses can still offset your other income under current rules while you hold them.[7, 9, 20]

- New established properties will have quarantined rental losses, so aggressive negative gearing is less attractive.[15, 17–18]

- New builds retain more traditional negative gearing benefits (plus the CGT discount), making them more likely candidates for higher LVRs and IO periods – if the asset quality stacks up.[3, 6, 14]

Loan structure helps you implement these different strategies side by side without muddling deductibility or reducing flexibility.

5.2 Estate planning and “what if something happens?”

Loan structure also affects what happens if you die or lose capacity.

From /insights/what-happens-large-home-investment-loans-when-you-pass-away: aligning loan structures, ownership entities and your will reduces disputes and lowers the chance of forced sales.

Practical steps:

- Avoid structures where the family home secures large investment loans.

- Keep clear loan schedules by property so executors can see which debt attaches where.

- Ensure buffers (offsets) and insurance (life, TPD, income protection) are sized to cover at least short‑term repayments while the estate is sorted.

5.3 Lender policy, buffers and APRA’s serviceability lens

APRA guidance currently expects lenders to assess most loans with at least a 3% serviceability buffer above the actual rate.

Implications for structure:

- Interest‑only loans are assessed as if they were P&I over the remaining term – this can constrain borrowing power.

- High LVR, multiple investment loans can quickly max out your serviceability even if your actual cashflow feels comfortable.

Flexible gearing means:

- Staggering fixed/IO expiry dates to avoid multiple step‑ups at once.

- Keeping enough offset balances and surplus income that you can pass tighter serviceability tests when you want to refinance.

- Considering how future rate rises or APRA policy shifts could change your ability to move lenders.

For a broader view on this, see /insights/mortgage-brokers-property-investors-portfolio-builders.

6. One‑week action plan to improve your structure

6.1 Day 1–2: Map your current structure

Create a simple spreadsheet listing for each loan:

- Lender and product name.

- Limit and balance.

- Interest rate and repayment type (P&I/IO, fixed/variable).

- Linked offset(s).

- Security property or properties.

- Purpose (home, investment, mixed; if mixed, estimate split).

Mark where cross‑collateralisation exists and where purposes are mixed in the same account.

6.2 Day 3–4: Identify pressure points and goals

Ask yourself:

- If I wanted to sell one property next year, how easy would that be under my current structure?

- Where is my non‑deductible debt sitting – and am I directing surplus cash there first?

- How many months of repayments do I hold in offsets across the portfolio?[16]

- Where will the negative gearing and CGT reforms likely hit my next purchase?

From this, set 2–3 priority goals, for example:

- Unwind cross‑collateralisation between home and investments.

- Create clear splits for investment‑purpose borrowings.

- Build buffers to 4 months of repayments within 18 months.

6.3 Day 5–7: Plan a staged restructure

Restructures work best in stages, often over months, not in one big bang.

Typical low‑disruption moves:

- Split existing loans with the current lender to separate purposes and attach offsets more logically.

- Refinance one investment at a time to move away from cross‑collateralisation or to sharpen pricing.

- Redirect surplus cash to the highest‑priority non‑deductible debt, while keeping your minimum buffer level intact.

- For self‑employed or complex situations, coordinate with your accountant to ensure the new structure aligns with entity and tax planning.

If your structure is heavily tangled, pair this guide with /insights/restructuring-loans-growing-property-portfolios to map out a 6–18 month roadmap.

FAQs

1. Is cross‑collateralisation ever a good idea for investors?

It can be acceptable in limited situations – for example, where equity is tight and one lender can only approve a transaction by securing multiple properties together. But it usually reduces your flexibility to refinance, sell or release equity later. If you use it, go in with a clear exit plan and monitor the structure as your portfolio grows.

2. How many offset accounts should an investor have?

You don’t need dozens of accounts, but having at least one offset linked to your home loan and, where possible, separate offsets for personal vs investment cash is helpful. The key is clarity: your broker and accountant should be able to tell at a glance which money relates to which purpose. Simpler is usually better as long as purposes stay distinct.

3. Should I put extra repayments into my home loan or investment loan first?

From a pure tax perspective, it usually makes sense to reduce non‑deductible home debt before tax‑deductible investment debt. However, you must keep enough buffer to manage risk on all properties. Using offsets rather than direct extra repayments can give you flexibility while still reducing interest on the targeted loan.

4. Do the negative gearing changes mean property investment is dead?

No. They change the after‑tax maths, especially for highly geared investors in established properties purchased after May 2026, but they don’t remove rental income or capital growth potential. The changes make asset quality, cashflow, and loan structuring more important, and are likely to shift demand toward new builds and other asset classes.

5. How often should I review my loan structure?

Aim for a formal review every 12–24 months, or sooner if a major life, income, rate or policy change occurs. Check your rates, structure, buffers, and whether your loans still match your goals. A review doesn’t always mean a refinance; often, small tweaks like new splits or re‑linking offsets can materially improve flexibility.

Key takeaways

- Flexible gearing starts with standalone, purpose‑clean loan structures, not whatever the bank defaulted to at settlement.

- Avoid or unwind cross‑collateralisation where possible so you can buy, sell and refinance property by property.

- Use offsets and loan splits deliberately to separate deductible from non‑deductible debt and maintain clear records.

- Aim for 3–6 months of repayments in offsets to keep your portfolio resilient to vacancies and rate or income shocks.

- Design your next move with the post‑2026 negative gearing and CGT rules in mind – especially whether a property is a qualifying new build or a non‑qualifying established dwelling.

- Review structures regularly and plan restructures in stages, aligning lending, tax and estate planning.

If you’d like help mapping and improving your current structure, book a free 15‑minute strategy call at https://localknowledge.finance. Your tax, your loan, one expert – a CPA, Tax Agent and Broker in one consultation, focused on keeping your gearing flexible and resilient.

General advice only.

Frequently asked questions

Is cross‑collateralisation ever a good idea for investors?▾

How many offset accounts should an investor have?▾

Should I put extra repayments into my home loan or investment loan first?▾

Do the negative gearing changes mean property investment is dead?▾

How often should I review my loan structure?▾

Speak with a specialist advisor

Confidential consultation, bespoke advice for your situation.