Article

Small business home loan eligibility: what lenders want to see

A clear, decision-grade guide to how Australian lenders assess small business owners and self-employed borrowers for home loans, and what you can fix this week.

Key Takeaway

Small business owners can qualify for Australian home loans if they show 1–2 years of stable, provable income, clean tax lodgements, and the capacity to afford repayments at an interest rate at least 3% higher than today’s (APRA’s serviceability buffer). Lenders usually start from taxable profit, adjust for add-backs, and compare income against HEM benchmarks. The most effective step within a week is to organise financials, separate business/personal cash flow, and map a suitable documentation pathway.

Self-employed business owners absolutely can qualify for a home loan, but eligibility rules are tougher than for employees. Lenders want to see (1) stable, provable income for at least 1–2 years, (2) clean, lodged tax returns, (3) a deposit of at least 5–20%, (4) a clear credit file, and (5) evidence you can afford repayments at your actual interest rate plus at least 3% (the APRA serviceability buffer). This guide walks through what that means in practice and what you can fix this week.

1. What is a “small business home loan” in practice?

There’s no separate product called a “small business home loan” at most banks. You’re applying for a standard home loan, but you’re assessed as a self-employed borrower rather than a PAYG employee.

The key differences:

- Your income comes from your business profits and drawings, not a payslip.

- Lenders scrutinise your business financials and tax compliance.

- Any business debts with personal guarantees are treated as your personal commitments.

- Volatile income is stress-tested harder because of the APRA 3% buffer.

For you, eligibility boils down to two stories:

- Personal story – your credit file, savings habits, living costs and existing debts.

- Business story – how stable, profitable and resilient the business is.

If both stories hang together, you’re in a strong position, even if your income is lumpy from month to month.

2. Core eligibility checklist for small business owners

Think of eligibility as a checklist. If you can confidently tick most of these, you’re close to application‑ready.

2.1 Personal profile

1. Residency and age

- Australian citizen or permanent resident (most lenders).

- At least 18 years old.

2. Deposit and equity

Indicative bands (can vary by lender and policy):

- 20% deposit (80% LVR) – best pricing, often no LMI.

- 10–15% deposit (85–90% LVR) – LMI likely, stronger income story needed.

- 5% deposit (95% LVR) – usually only with government guarantees or very strong profiles; documentation must be tight.

3. Credit history

- On‑time repayments for last 12–24 months.

- Minimal unsecured debts (credit cards, Afterpay, personal loans).

- Any defaults or judgements explained and ideally paid.

2.2 Business profile

Most mainstream lenders look for:

- Time in business: 2 years with ABN and GST registration (where relevant) is the sweet spot. Some will consider 1 year if the story is strong.

- Consistent or growing profit: Declining profit over two years is a red flag unless clearly explained.

- Separate accounts: Running business income and expenses through separate business accounts for 3–6 months usually boosts lender confidence (see /insights/separating-business-personal-cashflow-mortgage referenced fact).

- No unmanaged ATO debt: A small, documented payment plan can be workable; large undisclosed tax debt is often a deal‑breaker.

2.3 Income and serviceability

Two big concepts drive eligibility:

- Serviceability buffer (APRA rule) – Lenders must test if you can afford repayments at at least 3% above your actual rate. If your actual variable rate is 6%, they assess you at 9% or more.[^apra]

- HEM (Household Expenditure Measure) – A benchmark of minimum living costs based on your family size and location. Lenders take the higher of your declared expenses and HEM.

Combined with volatile income, that buffer (3) means self-employed borrowing capacity can be much lower than you expect from your top‑line revenue.

3. How lenders assess self-employed income

Every lender has its own policy, but the backbone is similar.

3.1 Structures: sole trader, company, trust

How your income is calculated depends on how your business is set up:

- Sole trader: Lenders start with net profit from your personal tax return.

- Company: They look at your salary + dividends + share of retained profit you can reasonably access.

- Trust: They assess the distribution to you plus any salary you draw.

In all cases, most lenders:

- Want two years of lodged tax returns (personal and business).

- Calculate income using either:

- the lower of the last year and 2‑year average, or

- latest year only if it’s clearly higher and sustainable.

For detail on how this plays out, see /insights/what-lenders-want-to-see-in-your-business-financials.

3.2 Tax returns, add-backs and deductions

Most lenders start from taxable profit and then add back certain items to reflect your real earning power:[^addbacks]

- Depreciation and amortisation – non‑cash expenses.

- One‑off or extraordinary costs – e.g. fit‑out, relocation.

- Some interest expenses – if those debts will be cleared or refinanced.

But there’s a catch:

Aggressively minimising taxable income can severely reduce your borrowing capacity, because lenders are not allowed to just accept your own “true income” estimate.

If you’ve been claiming heavily for a few years, it’s worth reading /insights/using-tax-returns-to-prove-income-home-loan before your next tax planning cycle.

3.3 Example: how assessable income is calculated

Say you run a company and your latest year shows:

- Your salary: $80,000

- Company taxable profit: $70,000

- Depreciation expense: $10,000

- One‑off legal fees (documented): $5,000

A lender might calculate your income roughly as:

- Salary $80,000

- Plus: profit $70,000

- Plus: add‑backs $15,000

- Total assessable income ≈ $165,000 p.a.

Another lender might be more conservative and use only salary + part of profit, especially if profit has been volatile.

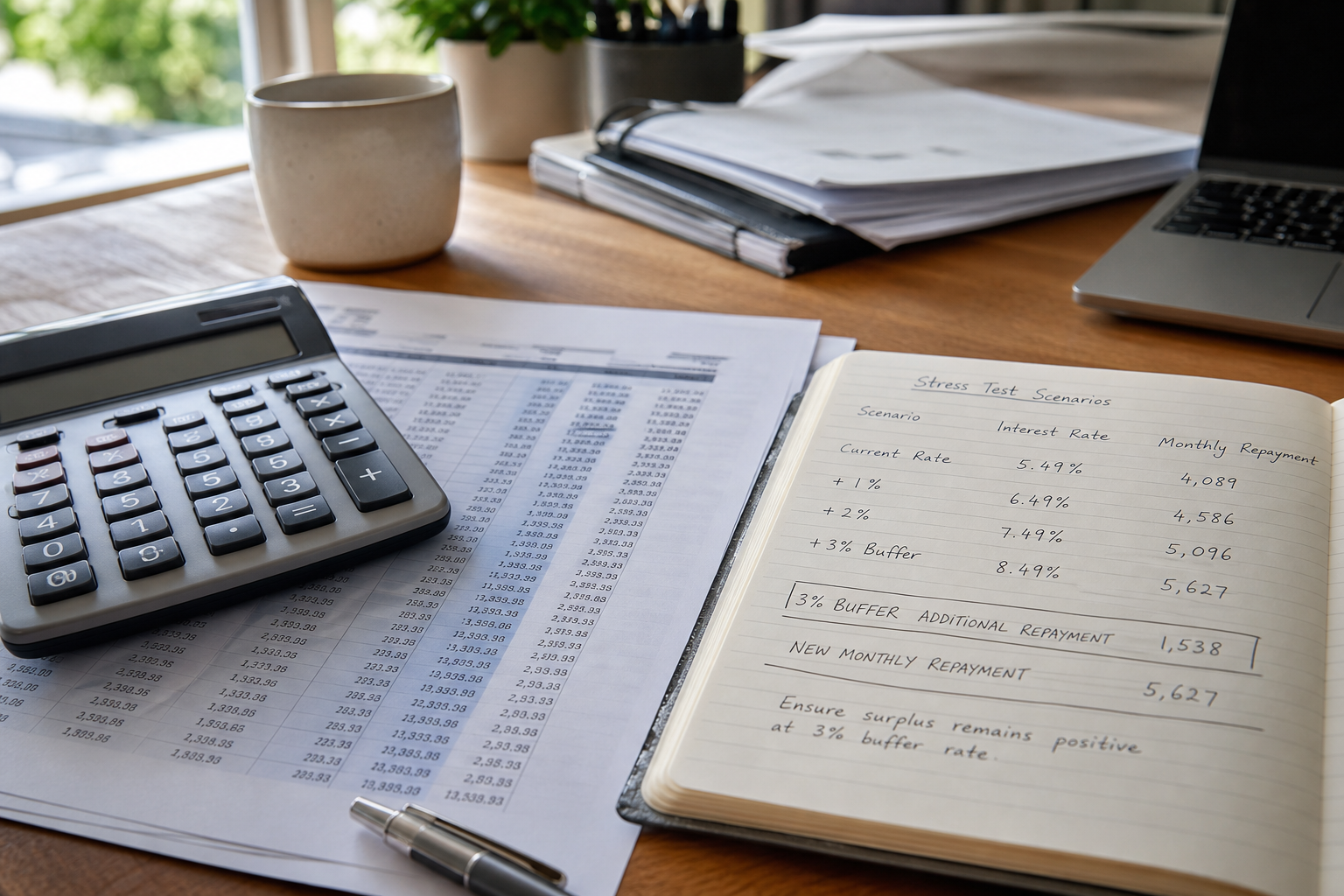

3.4 APRA buffer, HEM and borrowing capacity

Let’s take a simple example.

- You want to borrow $800,000 over 30 years, principal & interest.

- Indicative actual rate: 6% p.a. (illustrative only).

- APRA buffer: assess at 9% p.a.

Approximate repayments:

- At 6%: about $4,800 per month.

- At 9%: about $6,450 per month.

The bank will only approve the loan if, after allowing for HEM living costs and your other debts, your documented income comfortably covers $6,450 per month, not just $4,800. That’s why small dips in profit or extra credit cards can suddenly kill a deal.

With mortgage stress already affecting over 28% of Australian mortgage holders according to Roy Morgan’s 2026 research, regulators and banks are in no mood to be generous with these tests.

4. Documentation pathways: full-doc, alt-doc and low-doc

The way you prove income – your documentation pathway – has a big impact on eligibility, LVR and pricing.

For a deeper dive, see /insights/documentation-pathways-full-doc-alt-doc-low-doc-options. Here’s the short version.

4.1 Full-doc (cheapest if you qualify)

Best for: Established, profitable businesses with clean tax lodgements.

Typical requirements:

- 2 years personal tax returns and Notices of Assessment.

- 2 years business tax returns and financial statements.

- Latest BAS statements and business bank statements.

- ATO portal screenshot confirming no major outstanding tax.

Pros:

- Access to most lenders and the sharpest pricing.

- Higher maximum LVRs (often up to 90–95% with LMI, depending on policy).

Cons:

- If your tax returns show low profit (because of deductions), your borrowing capacity may be limited.

4.2 Alt-doc (flexible proof, moderate pricing)

Best for: Strong businesses where tax returns don’t reflect current income (e.g. rapid growth, recent restructure).

Proof of income may rely on:

- 6–12 months of business bank statements.

- 2–4 quarters of BAS.

- An accountant’s letter confirming sustainable income.

Pros:

- More aligned with current trading performance.

- Helpful if you’ve only recently started paying yourself a higher, stable salary.

Cons:

- Often slightly higher rates and fees than full‑doc.

- May require larger deposit (e.g. capped at 80% LVR).

4.3 Low-doc (niche, last-resort option)

Low-doc is now a small, specialist niche.

- Often needs large deposits (20–30%+).

- Rates can be materially higher.

- Tight policy around credit history.

For most serious small business owners, the goal is to move towards full-doc or strong alt-doc over 6–24 months by tidying your financials and tax planning.

5. Deposit, LVR and LMI: what’s realistic for small business owners?

Lenders don’t just look at your deposit percentage; they look at where it came from and how it affects your business.

5.1 Source of deposit

Stronger:

- Genuine savings built over 3–6+ months.

- Sale of another property or other assets.

- Gift from immediate family (with a declaration).

- First Home Super Saver (FHSS) releases and government grants for eligible first‑home buyers.

Higher risk:

- Large withdrawals from business working capital.

- Delaying or underpaying tax to fund the deposit.

- Short‑term loans or credit card cash advances.

As noted in /insights/how-lenders-really-view-your-small-business-home-loan, draining business cash for a deposit can weaken your case, because it reduces your resilience to revenue shocks.

5.2 Comparison: PAYG vs self-employed vs alt-doc

Below is an illustrative comparison only – real policies and pricing vary by lender and over time.

| Borrower type | Typical max LVR* | Likely doc type | Indicative pricing band** | Key conditions |

|---|---|---|---|---|

| PAYG employee, clean file | 95% (with LMI) | Full-doc | Lowest available | Stable job, standard expenses |

| Self-employed, strong full-doc | 90–95% (LMI) | Full-doc | Close to PAYG | 2 yrs financials, good profit |

| Self-employed, alt-doc | 80% (sometimes 85%) | Alt-doc | Moderate premium | Strong bank/BAS history, clean credit |

| Self-employed, low-doc | 60–80% | Low-doc | Highest | Large deposit, strong security needed |

* Subject to lender policy and LMI provider.

** Pricing bands are indicative only – no specific rates are quoted.

For many small business owners, a realistic, sustainable target is 80–90% LVR, balancing deposit effort, LMI cost and business cashflow.

6. Common red flags and deal-breakers

Understanding what spooks lenders lets you fix problems before you apply.

6.1 Tax debt and late lodgements

- Unlodged returns: Many lenders will not proceed until all required returns are lodged. Late lodgements also hint at poor financial control.

- Large ATO debts: A tax bill sitting unpaid (or on a shaky payment plan) is often viewed as more serious than a normal personal loan.

If you have tax issues, tackle them months before you apply. A broker who is also a tax agent can help you work through the sequence.

6.2 Business debts and personal guarantees

In Australia, most lenders treat business facilities with personal guarantees as personal commitments, even if repayments are coming from the business account.[^guarantees]

That means:

- Business overdrafts, equipment finance, and secured business loans often count in your serviceability.

- Rolling these into a home loan can improve short‑term cashflow, but increases exposure of your family home if things go wrong.

Structured well, some debts can be shortened and quarantined (e.g. using a separate home loan split with a 5–10 year term), but this needs careful tax and credit advice.

6.3 Using business cash for your deposit

Tempting but risky:

- Pulling $80,000 out of working capital for a deposit might get you to 80% LVR.

- But if that leaves your business unable to ride out a 3–6 month slump, lenders see higher risk – and they’re right.

Remember, self-employed borrowers usually need both a personal buffer and a separate business buffer to protect the family home.

6.4 Overly complex structures you can’t explain

Multiple companies, trusts and related‑party loans aren’t an automatic problem, but they need a clear, simple explanation:

- Who owns what?

- Who owes what?

- Where does your actual living income come from?

If you can’t explain it in one page, the credit assessor will probably say no.

7. A one-week plan to get closer to approval

You don’t need to fix everything this week, but you can dramatically improve your position with focused action.

Day 1–2: Get your numbers in front of you

- Download the last 6–12 months of bank statements for both personal and business.

- List all debts: credit cards (limits and balances), personal loans, car leases, business loans and overdrafts.

- Pull a free credit report to check for surprises.

If you’re a first‑home buyer running a business, cross‑check your situation against /insights/first-home-buyer-small-business-owner-guide for grant and guarantee options.

Day 3–4: Tidy your income story

- Make sure at least the last two years of tax returns are lodged (or get a plan to lodge them quickly).

- Work with your accountant to identify legitimate add-backs (depreciation, one‑offs).

- Start paying yourself a consistent, conservative “salary” from business to personal – weekly or fortnightly – to smooth income.

If your returns don’t reflect current income, skim /insights/home-loans-high-income-self-employed-professionals for strategies to align your structure and borrowing goals.

Day 5: Separate and simplify cashflow

- If you’re still mixing business and personal spending, open a separate business account and start running all business income and costs through it.

- Close unused credit cards and reduce unnecessary limits.

Over 3–6 months, this separation usually lifts lender confidence and makes your real living expenses much clearer.

Day 6: Start building your buffers

Roy Morgan’s data shows more than one in four mortgage holders are already at risk of stress. As a business owner, your margin for error is thinner.

- Calculate at least 6 months of bare‑bones personal expenses.

- Add 3–6 months of business fixed overheads (rent, insurances, minimum wages).

- Set up separate emergency accounts and automate transfers, even if small to start.

For a step‑by‑step method, see /insights/build-six-twelve-month-buffer-before-mortgage.

Day 7: Map your documentation pathway with a specialist

Small business owners benefit from a broker who understands tax, business structures and lender policy, not just interest rates. A specialist can:

- Estimate your borrowing capacity under full-doc vs alt-doc.

- Flag any deal‑breakers before you hit submit.

- Suggest whether to apply now or wait for another BAS or financial year.

/insights/mortgage-brokers-self-employed-professionals-small-business-owners explains exactly how this kind of broker works and what you can realistically get done in a week.

8. Putting it together: are you likely to qualify?

You’re probably close to eligible if:

- You’ve been in business 2+ years with lodged tax returns.

- Business profit is stable or growing.

- You have a 10–20% deposit that doesn’t cripple working capital.

- Your credit is clean and your debts are under control.

- You can build or already hold 6–12 months of buffers (personal + business).

You may need more work (or a staged plan) if:

- Profit has dropped significantly year‑on‑year.

- You have large ATO debts or unlodged returns.

- Most of your deposit would come from draining business reserves.

- Your structure is complex and your accountant can’t easily summarise your position.

In those cases, the smart move is often to delay the application slightly, fix the weak points, and then apply once your story is stronger.

FAQs: small business home loan eligibility

1. How long do I need to be in business to get a home loan?

Most lenders want at least 2 years of self-employment with lodged tax returns. Some will consider 1 year if you’re in the same industry you previously worked in as an employee and your numbers are strong. Shorter histories usually mean fewer lender options and more conservative borrowing limits.

2. Can I get a home loan with only one year of financials?

It’s possible but harder. You’ll usually need to show strong current trading using BAS and bank statements, be in a field where your prior PAYG role is clearly relevant, and have a solid deposit. Expect tighter LVR caps and more questions from credit, and consider whether waiting for a second year of financials would materially improve your options.

3. How do banks treat my business debts when assessing my home loan?

If a business loan, overdraft or lease has your personal guarantee, most lenders treat the repayments as your personal commitments. Even if the business pays them, they reduce your borrowing capacity. A broker can sometimes restructure or shorten these debts to improve your position, but they can’t simply be ignored.

4. Will all my tax deductions hurt my borrowing power?

Legitimate deductions are fine, but very aggressive tax minimisation usually cuts your borrowing capacity because lenders work from taxable profit. You and your accountant may decide to show slightly higher taxable income for a year or two if a home purchase is on the horizon. The key is planning this ahead of time rather than after the tax return is lodged.

5. Is an alt-doc home loan safe for my business?

Alt-doc is a normal, regulated type of lending that simply uses different income documents. The main trade‑offs are slightly higher rates, often lower maximum LVRs, and a narrower range of lenders. It can be a useful bridge if your business is growing fast, but your medium‑term goal should usually be to transition to full-doc once your financials catch up.

6. Can I use my home loan to fund business expenses or equipment?

You technically can, but it’s often not ideal. Using 30‑year home loan debt to fund short‑lived business assets usually increases total interest costs and concentrates business risk on your family home. In many cases, a properly structured short‑term business loan or equipment finance is safer and more tax‑efficient.

Key takeaways

- Small business owners can absolutely get home loans, but lenders scrutinise tax returns, business stability and personal buffers far more closely than for PAYG borrowers.

- APRA’s 3% serviceability buffer and HEM benchmarks mean your borrowing capacity is based on conservative assumptions, not best‑case income.

- Documentation pathway (full-doc vs alt-doc) shapes your maximum LVR, pricing and lender choice, so it’s worth planning 6–24 months ahead.

- Avoid draining business cash or carrying large ATO debts into your application; both can significantly weaken your case.

- Within a week you can organise your numbers, separate cashflow, start buffers and map a lending strategy with a specialist who understands both tax and credit.

Ready to see what’s realistically possible for you? Book a free 15‑minute strategy call at localknowledge.finance. In one conversation you’ll get your borrowing capacity estimated, red flags identified, and a clear plan that aligns your business, tax and home goals — your tax, your loan, one expert: a CPA + Tax Agent + Broker in one consultation.

General advice only.

Frequently asked questions

How long do I need to be in business to get a home loan?▾

Can I get a home loan with only one year of financials?▾

How do banks treat my business debts when assessing my home loan?▾

Will claiming lots of tax deductions hurt my home loan borrowing power?▾

Is an alt-doc home loan risky for self-employed borrowers?▾

Should I use my home loan to fund my business or equipment?▾

Speak with a specialist advisor

Confidential consultation, bespoke advice for your situation.